.svg)

Don’t Throw Away Your Innovation Budget

With threats looming from every direction, it can be tempting to make precautionary investments in innovation. All too often, though, companies bet on new projects without thinking through how they will integrate with current offers and teams. That's like running a water main up to your house, then not connecting it to your plumbing. Yes, you’ll have water, but you won’t be able to channel it toward anything useful.

This lack of contextual thinking and foresight is why so many innovation investments fail—it’s not for lack of ingenuity, but because companies build innovation teams, then neglect to design a complete ecosystem to take promising ideas forward.

Here are the three most common traps that cause even the smartest business leaders to throw their innovation money away:

1. The Outcome Trap — If you don’t define a clear vision for how innovation is supposed to contribute to your company’s growth, don’t be surprised when innovation teams fail to make a contribution.

2. The Incentive Trap — No one wants to play Russian roulette with their career. If you don’t incentivize business units to make the right mix of bets, they’ll have no reason to invest in anything other than short term sure things.

3. The Metrics Trap — Success isn’t subjective. If you don’t create innovation metrics that the rest of the organization can understand, the rest of the business may view innovation as frivolous.

The Outcome Trap

About 10 years ago, a parcel courier (one of those companies that brings cardboard boxes to your door) built an innovation unit to help power their future. Senior executives had held inspiring conversations and decided that “innovation” would build the future of their company, so they built a new team and recruited a former startup guy to run it. Everyone had high hopes for the team’s success.

What happened next? The startup guy built them a startup. The team found some cool technology and a strong customer need. They used that to build, launch, and sell a profitable new solution to a small but growing pool of customers.

Was it a success? Well, only to some stakeholders. When the team began to share their results, they faced surprisingly hostile reception: One senior executive wanted to know when the innovation division was going to yield strategic insights for the core company. Another asked when it would start developing new technologies for the core business. A third wondered when it would train her teams in innovation. Despite some wins in the market, few stakeholders were happy with the results. Within 18 months of their launch, they were disbanded.

This company fell into a surprisingly common trap: Everyone thought that “innovation” was important, but nobody ever talked about why they wanted it. It was like the execs had asked a waiter for ice cream and then got upset when their server showed up with Rum Raisin.

So, how can you avoid the Outcome Trap?

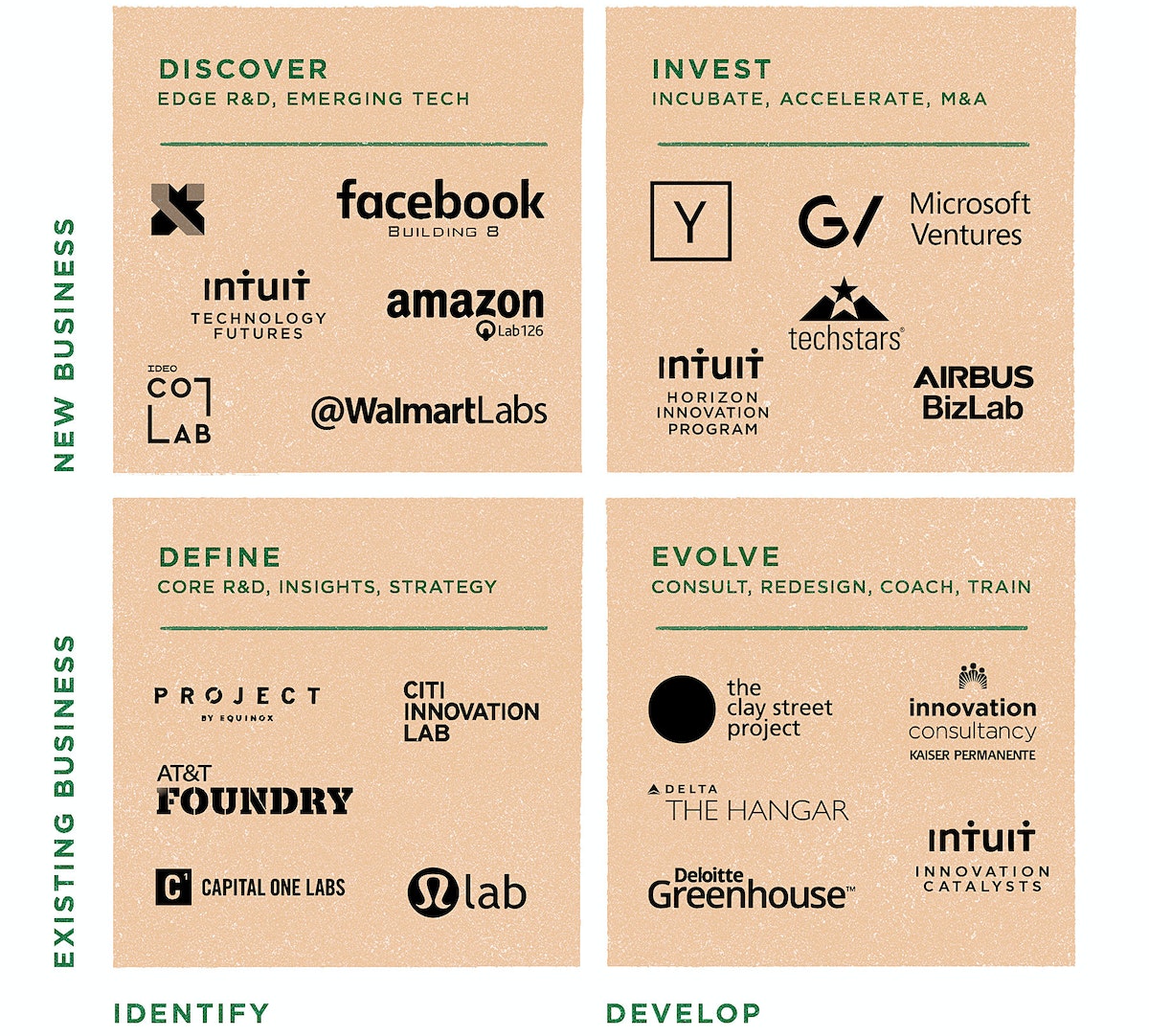

Work backwards. First, define why innovation is important and why now. Once you define the outcomes needed from innovation, you can craft a portfolio of projects designed to meet those goals. That portfolio then suggests the talent, skills, and even the number of people or teams you’ll need to drive innovation. When we break them down, successful innovation portfolios consist of a mix of four activities.

In the graphic below, we’ve plotted businesses and teams based on our evaluation of their primary objective (even though many of these teams invest in more than one quadrant).

As shown in the above graphic, Discover teams focus on uncovering new insights or opportunities that could be developed into new businesses or offers. This long-term innovation work includes the efforts of R&D labs focused on emerging technology. Those in the Invest quadrant develop, launch, or acquire new businesses in the short term. This includes the work of M&A teams, accelerators, incubators, and corporate venture capital. Define teams initiate tangible strategic visions for how existing business units may need to evolve to succeed in the future, and reveal opportunities for how current offers can adapt to changing customer demands or new technologies. And lastly, Evolve teams differ in that they partner with existing business units to adapt to a changing environment—develop new offers, approaches, and skills to improve the business in the near- to mid-term. This includes the services offered by SWAT teams, internal agencies, and coaches.

By intentionally balancing the portfolio—say, by focusing sharply on incubating new digital ventures and adapting current offers—the innovation team can define their projects, align their stakeholders, and allocate their staff.

The above graphic highlights the shape of a lab portfolio at a successful retail conglomerate—80% of their efforts are focused on either evolving the current subsidiaries or helping those subsidiaries invest in new digital ventures. The remaining 20% of their effort goes into defining future strategy and discovering new tech to harness.

—

To avoid this trap, ask yourself: Why innovation, and why now? What does success look like? What’s the future vision for our company, and how should innovation contribute to that? Where are we facing the biggest market threats—in the short term or the long term? Will innovation provide services to core business units or will it build new subsidiaries? Your innovation portfolio and your teams will naturally evolve over time, but you can control that evolution by intentionally defining the purpose of the team and the outcomes that they need to deliver.

The Incentive Trap

Once you’ve defined the ideal innovation portfolio, you need to find the right sponsors willing to make the right bets on the right projects. The best strategy is doomed if no one has any incentive to make good bets. That’s the Incentive Trap.

Several years ago, a global home appliances company created a Lifestyle Research Lab to design new products that address consumers’ changing attitudes and behaviors. In isolation, the team conducted their own research and used it to develop new ideas that could transform their white goods businesses—creating radically new dishwashers, refrigerators, or washing machines. When they hit on a juicy idea, they would then try to sell it to a business unit for development.

Now, imagine yourself leading one of those businesses: One day, out of the blue, someone you’ve never met pitches you on a new product. Based on some research you’ve never seen and some shiny concept sketches, this team insists that you should change up your five-year product development roadmap. You didn’t ask for this idea, you didn’t pay for this work, and their analysis doesn’t match up with the numbers that you normally track. Your budget, your people, and your manufacturing are already committed. Even if you love their idea, you’d need to do a lot of heavy lifting to justify changing your plans. Few executives at the appliance company were willing to do that work.

Looking at the innovation portfolio and the purpose that’s been defined, what kind of bets should business units to make?

In a completely rational world, a decision between investing on a sure thing or a smart bet should be a toss up. However, to many executives, investing in riskier projects can feel like career Russian roulette. In your own company, how much of a balance do you have between sure things and smart bets?

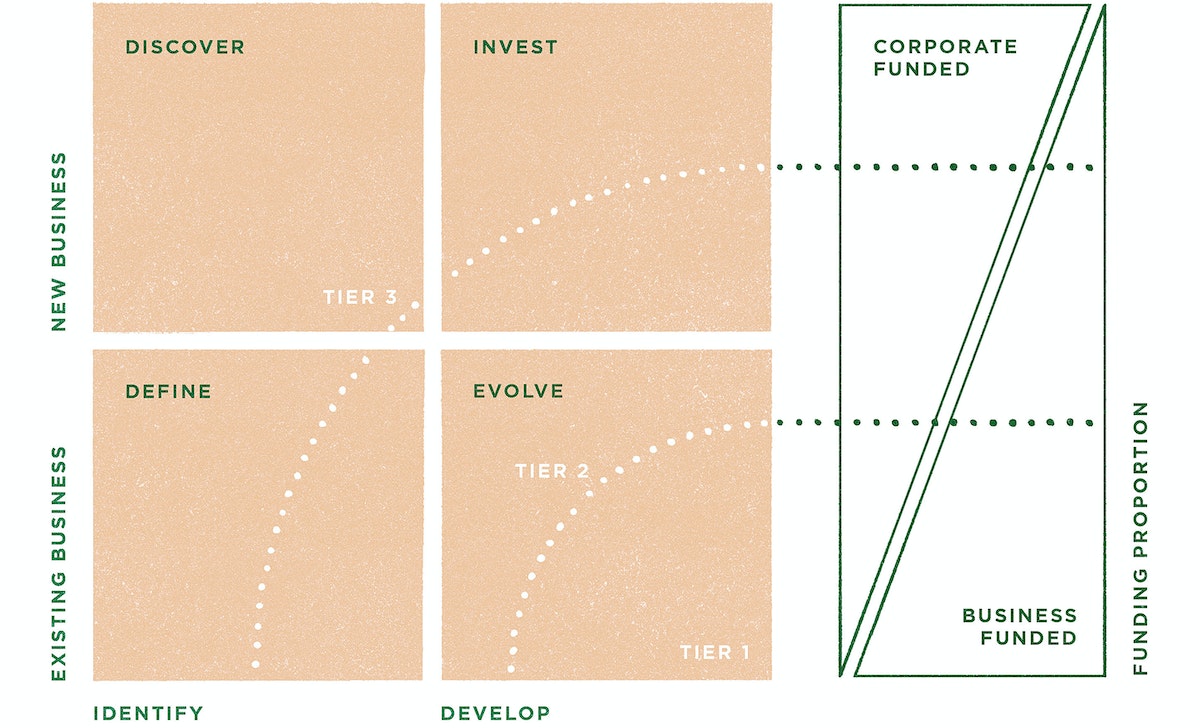

To create a more balanced mix of bets, many companies fund innovation from some central, corporate pool. This promotes riskier bets—it’s always easier to gamble someone else’s money. But there’s a catch: when the business units pay too little for innovation, they don’t value the work. Business leaders can see this kind of innovation as a sideshow. When the going gets tough, and those business leaders need to improve their metrics, they will kill any innovation projects that aren’t yet proven.

So, what happens when a business unit pays the tab? Although leaders are more invested in the outcomes (literally and figuratively), their demand for innovation is far lower. When betting their own money, most people prefer sure things—even when the expected returns are the same, they choose an option that’s easier to predict. So, how do you promote riskier bets? With corporate funds. We often see these corporate subsidies falling into three tiers. This model isn’t just true for how business units spend their money, it’s also true for how they assign their best people. They aren’t likely to put their best people on their riskiest projects.

The above graphic illustrates that as you define your portfolio, you’ll also need to define a funding mix for the work that incentivizes the right bets. The incentives tend to fall into three tiers: Tier 1 investments feel more like sure things; tier 2 investments feel a little riskier, but still appealing; tier 3 investments feel too risky to make without senior executive support.

—

To avoid this trap, ask yourself: Looking at your ideal portfolio, what is a healthy mix between sure things and smart bets? How adventurous are your business units, and how much do you need to incentivize their investments? The more corporate pays, the more risk business units will take on.

The Metrics Trap

Once you make your bets, how do you know if they’re paying off? If innovation isn’t seen to create measurable value, it’s worthless. That’s the Metrics Trap.

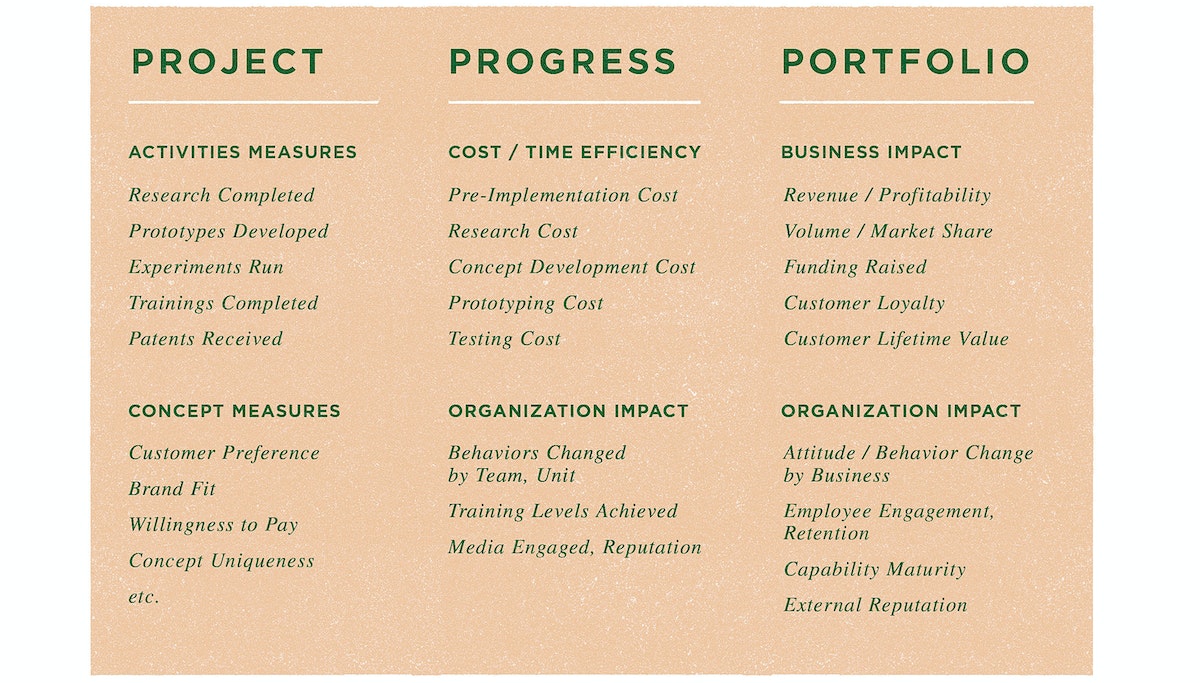

One sneaky reason that so many companies throw away good money on bad innovation efforts is that innovation may take years to show impact on metrics that the business units typically track, like revenue, profit, lifetime value, or customer satisfaction. But that doesn’t mean that innovation teams can’t show value in the short term. By setting simple baselines, teams can measure progress over time, showing that their work improves outcomes, drives efficiency, or changes behavior. These progress measures demonstrate indisputable value, and can often satisfy skeptical stakeholders in the short term—until innovation’s portfolio of work hits the market and begins to generate real growth.

To properly measure both the productivity of individual projects and the performance of the overall investment strategy, many innovation units build a basket of metrics that they can track in various timescales, as captured in the diagram above.

One global financial services company has taken some smart steps to avoid the Metrics Trap. They built a Fintech Incubator to develop new digital offers on behalf of the bank’s business units. Before the Incubator will take on a project, a sponsoring business unit must make a business case for the product, put up a majority of the development costs, and define a series of success criteria for further investment. This aligns the innovation process with the business unit’s needs. On top of those project metrics, the incubator’s leaders also track a set of progress metrics across all of their work. These measures demonstrate how, over time, the incubator is moving down the cost curve. They’ve used progress measures as an argument for how the core business should rethink the way that they build and test new concepts.

—

To avoid this trap, ask yourself: Once you make your bets, what metrics will you use to calculate whether they’re paying off? What does your business value? What will you measure in various timescales to demonstrate the success of your projects, your progress, and your portfolio?

These aren’t the only innovation traps, but they are the deadliest. Innovation should not be a game of Russian roulette. By carefully considering and designing solutions to each trap, you can get that much closer to crafting an investment portfolio and innovation ecosystem that can nurture the future of your company.

Visuals by Gracia Lam.

Words and art

Subscribe